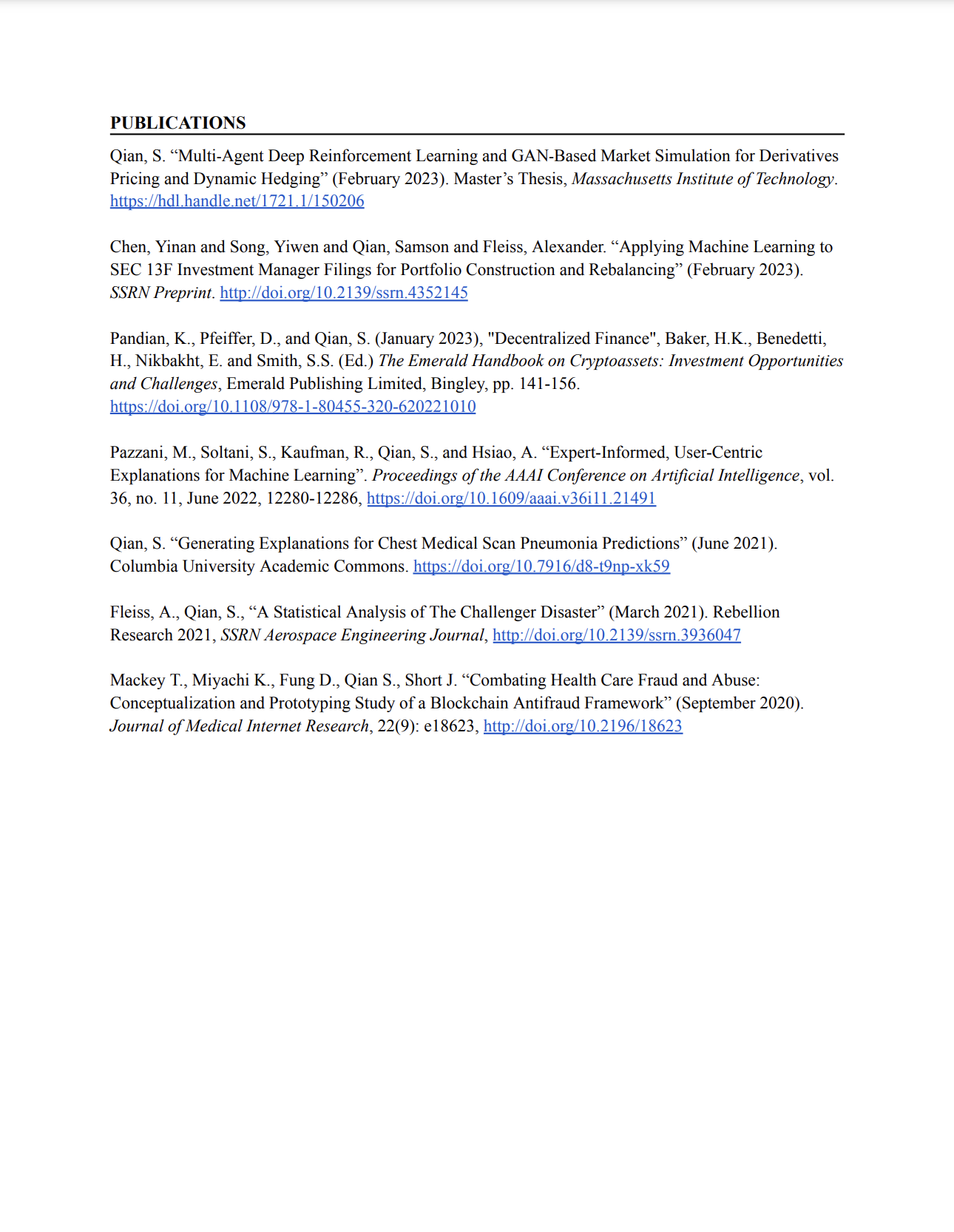

Samson Qian

About Me

Samson holds a Master of Finance degree from the MIT Sloan School of Management and a B.S. degree from the University of California, San Diego in data science. At MIT, he was the president of Sloan’s Quantitative Finance Club and hosted the 2022 MIT Sloan AI & Quant Conference. He is also affiliated with various A.I. and DeFi organizations. He has worked in various research groups and has done extensive research in machine and deep learning methods, blockchain and web3.0, and quantitative finance. His experience mainly lies in working on quantitative research and data science teams in financial services firms to research and develop quantitative methods to support systematic investment strategies, market analysis, and risk management.

Resume

Research

Samson’s MIT thesis “Multi-Agent Deep Reinforcement Learning and GAN-Based Market Simulation for Derivatives Pricing and Dynamic Hedging” explores how GANs can be used as an alternative non-parametric approach to simulate and generate market data, as opposed to traditional Monte-Carlo methods that rely on assumptions about underlying distributions. This systematic framework becomes applied to deep hedging algorithms to train agents to find the optimal hedging policy. This deep reinforcement learning-based approach makes the dynamic hedging strategies more robust and precise compared to traditional greek hedging.

TEDxBoston